Q&A with Investment Strategy: Tariffs and Retaliation

Tariffs & Retaliation

March 4, 2025

Larry Adam, Chief Investment Officer

Eugenio Alemán, Chief Economist

Pavel Molchanov, Investment Strategy Analyst

HOW ARE FOREIGN GOVERNMENTS RESPONDING TO TRUMP’S TARIFFS?

Now that US import tariffs and corresponding retaliatory measures have moved from rhetoric to reality, markets around the world are reacting. A look back at the first Trump term shows that retaliation against US tariffs had a negative effect on some sectors of the US economy, particularly agriculture. What the US government paid out in farmer relief payments canceled out the Treasury’s tariff revenue. And whereas the original Trump tariffs took place while the US was fighting deflationary forces, today’s environment is quite the opposite as inflationary pressures are still elevated.

A REMINDER: WHAT TARIFFS HAS THE TRUMP ADMINISTRATION IMPOSED?

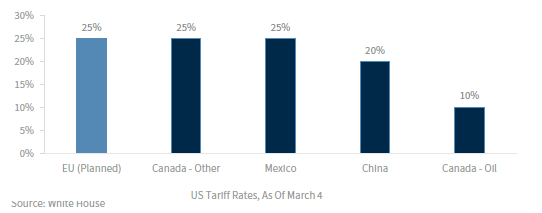

The second Trump administration is more forceful than the first as it relates to imposing import tariffs. Compared to the Trump 1.0 approach of targeting tariffs vis-à-vis specific industries, the major tariffs imposed over the past six weeks encompass all imports from America’s four largest trading partners: Canada, Mexico, China, and the European Union. (Of these, all have already taken effect, except the EU.) This means that 61% of US imports have or will be covered by tariffs ranging from 10% to 25%, as shown below. In addition, there are targeted tariffs of 25% on steel and aluminum that come into effect on March 12.

HOW ARE FOREIGN GOVERNMENTS RETALIATING?

When a 10% across-the-board tariff on imports from China took effect on February 4, China’s initial response was mild: it imposed tariffs on select US products, crude oil, LNG, and coal, as well as heavy machinery. In addition, China placed restrictions on exports of several strategic metals, such as molybdenum. With the tariff doubling to 20% on March 4, China’s response escalated as well: tariffs of 10% to 15% on US agricultural products, including the most economically important one: soybeans.

With regard to the EU, Canada, and Mexico, the response is likely to be different. As an agricultural exporter itself, the EU buys only small amounts of agricultural products from the US. On the other hand, the EU is the largest importer of US natural gas, especially since Russia’s invasion of Ukraine in 2022. Canada and Mexico have the closest linkages to the US economy, so they are able to impose tariffs on a wide range of US products. Canada has compiled a C$155 (US$108) billion list of US products subject to 25% retaliatory tariffs, of which one-fifth took effect on March 4. Mexico plans to unveil its response this coming Sunday.

In crafting their response, governments abroad are well aware of how US politics works. They are able to focus retaliation against industries—notably, agriculture—that happen to be prevalent in Republican (‘red’) states as a way of shaping public opinion in communities that would otherwise be supportive of Trump.

WHY IS THE US AGRICULTURAL SECTOR VULNERABLE TO RETALIATORY TARIFFS?

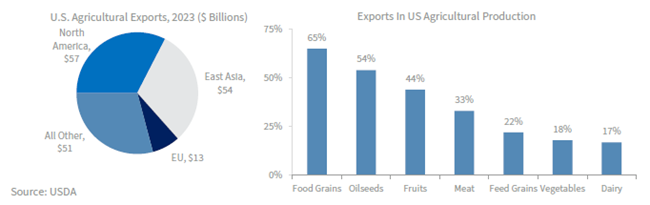

The US is the world’s largest agricultural exporter in absolute terms. Since the 19th century, the US agricultural sector’s productivity has been such that there are ample surpluses available for export. On average, 20% of US agricultural output is exported, though this percentage varies a great deal depending on the product, as shown below on the right. US agricultural products are sold all over the world. China is the number one destination of US agricultural exports, though it is topped by Canada and Mexico combined. US sales to China are dominated by soybeans—a vital input for China’s animal farms. Brazil and Argentina are probably going to benefit the most if China decreases soybean purchases from the US.

WHAT DO WE KNOW ABOUT CHINA’S RETALIATION FROM TRUMP’S FIRST TERM?

As the Chinese government targets the US agricultural sector, this is a replay of its playbook from 2018-2019. At that time, China imposed tariffs on US agricultural products—and, in some cases, halted purchases entirely. For example, China’s purchases of US ethanol (made from corn) fell to virtually zero in 2019.

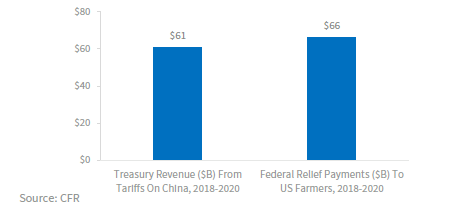

In response to the economic hardship suffered by US farmers as a result of China’s retaliation, the Trump administration proposed, and Congress approved, several packages of relief payments. As shown above, these relief payments totaled $66 billion, which essentially matched how much revenue the US Treasury collected from tariffs on Chinese imports during the same timeframe. In other words, there was no budgetary benefit for the federal government—all the tariff revenue went to compensating farmers. As we explain on the next page, there is reason to believe that it would be a similar story this time around—except on an even larger scale.

HOW MANY US JOBS ARE AT RISK FROM RETALIATION?

US Department of Agriculture data shows that 2.6 million Americans work on farms, which equates to slightly more than 1% of the total US workforce. As we noted earlier, approximately one-fifth of US agricultural production is exported, and—proportionally—480,000 farming jobs are tied to exports. Because of what the USDA calls agricultural trade multipliers, exports have read-through across the economy: for example, fertilizer distributors who supply farms, underwriters who issue crop insurance policies, and truck drivers who deliver goods to seaports. The USDA estimates that an additional 770,000 jobs outside the agricultural sector are supported by exports. In total, 1.2 million jobs could be adversely affected, to some degree, by tariff-related retaliatory measures.

HOW IS THE TRADE WAR AFFECTING BROADER ECONOMIC ACTIVITY?

When we zoom out for a broad perspective, what we can see is that tariffs are being used by the Trump administration as a means to address a wide range of issues. Some are purely economic, such as foreign tariffs on US products, or unfair competitive practices. Others are essentially non-economic, such as attempting to achieve progress on illegal immigration and drug trafficking across US borders.

Our sense is that diplomats, both in the US and abroad, are struggling to figure out how to address the Trump administration’s non-economic demands. Whereas trade deficit/surplus metrics are straightforward to measure, the non-economic demands are difficult to quantify. While diplomats try to figure all of this out, US businesses may have to navigate around higher costs. As we already saw with the preliminary goods trade deficit in January, businesses in the US have moved ahead and tried to preempt higher tariffs by increasing imports considerably. This has increased the trade deficit in goods, and it threatens to shift the economic conversation from an expanding economy to a temporarily weakening or even contracting economy during the first quarter of this year, which will likely be short-lived.

THE BOTTOM LINE

As the Trump administration pursues its tariff agenda, retaliation by foreign governments is already underway, and more is likely to come. Initial signs point to the US agricultural sector being a prime target for retaliation, just as it was in 2018-2019. In the meantime, investors should avoid overreacting to daily tariff headlines, as negotiations can quickly lead to reversals. Rest assured, we will keep our readers updated as events unfold.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC. Reynolds Wealth Management is not a registered broker/dealer and is independent of Raymond James Financial Services. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. This information is intended to be educational and is not tailored to the investment needs of any specific investor. Every investor's situation is unique, and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.

All expressions of opinion are those of Investment Strategy and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

SECTORS | Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.

COMMODITIES | Investing in commodities such as copper is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

ENERGY COMMODITIES | Investing in energy commodities is generally considered speculative, with high levels of volatility, limited market regulation, and emerging markets risk. Oil prices are influenced by OPEC decisions and tend to be economically sensitive. Natural gas prices are influenced by weather.

© 2025 Raymond James Financial Services, Inc., member FINRA/SIPC.